The global electronic music industry is still growing—but the way it grows is changing.

According to the latest IMS Electronic Music Business Report, an annual study of the electronic music industry by Mark Mulligan and MIDiA Research for IMS Ibiza, the sector reached a value of $15.1 billion in 2025, marking a 7% increase year-on-year.

On the surface, that signals another strong year. Underneath, however, the dynamics driving that growth are shifting in ways that say a lot about where the wider music industry is heading.

DOWNLOAD THE FULL REPORT HERE

Growth Is Steady—But Not Uniform

Electronic music continues to benefit from the same forces shaping the broader music business: streaming, global expansion, and digital consumption. Subscriber growth remains strong, with global streaming users increasing significantly—driven largely by emerging markets in the Global South.

At the same time, streaming is no longer the uncontested growth engine it once was. For the first time, streaming grew slower than the overall market, a signal that other revenue streams are starting to play a more important role. This does not mean streaming is declining—it remains central—but it does suggest that the industry is entering a more complex phase.

The Fan Economy Takes Center Stage

One of the clearest signals in the report is the rise of what MIDiA defines as “expanded rights”—including merchandise, direct-to-consumer sales, and other fan-driven revenue streams. In 2025, this segment grew by 21%, outperforming all other areas of the recorded music business. This shift reflects a broader industry transition: from monetizing access to monetizing engagement. Electronic music is particularly well positioned here. Its culture has always been rooted in scenes, identity, and community—elements that translate naturally into deeper fan relationships and alternative revenue streams.

Live Music: Growth with Constraints

Live music remains a key pillar of the electronic ecosystem, continuing its post-pandemic recovery. Revenues from major live companies reached $30 billion in 2025, more than double pre-pandemic levels. However, the nature of that growth is worth noting. Much of the increase is being driven by higher ticket prices rather than higher attendance, with ticket sales in some markets, such as the US, actually declining. This suggests that while demand remains strong, there may be limits to how far pricing can continue to carry growth.

AI Is Reshaping the Creation Layer

While much of the conversation around AI in music focuses on copyright and distribution, the report highlights a different—and arguably more immediate—impact. AI is transforming how music is created. Revenues from generative AI and stem separation tools grew by 651% between 2023 and 2025, reaching $333 million, with 63 million monthly active users. This represents a structural shift. Music creation is becoming more accessible, lowering barriers to entry and expanding the creator economy—while also increasing content supply at an unprecedented pace.

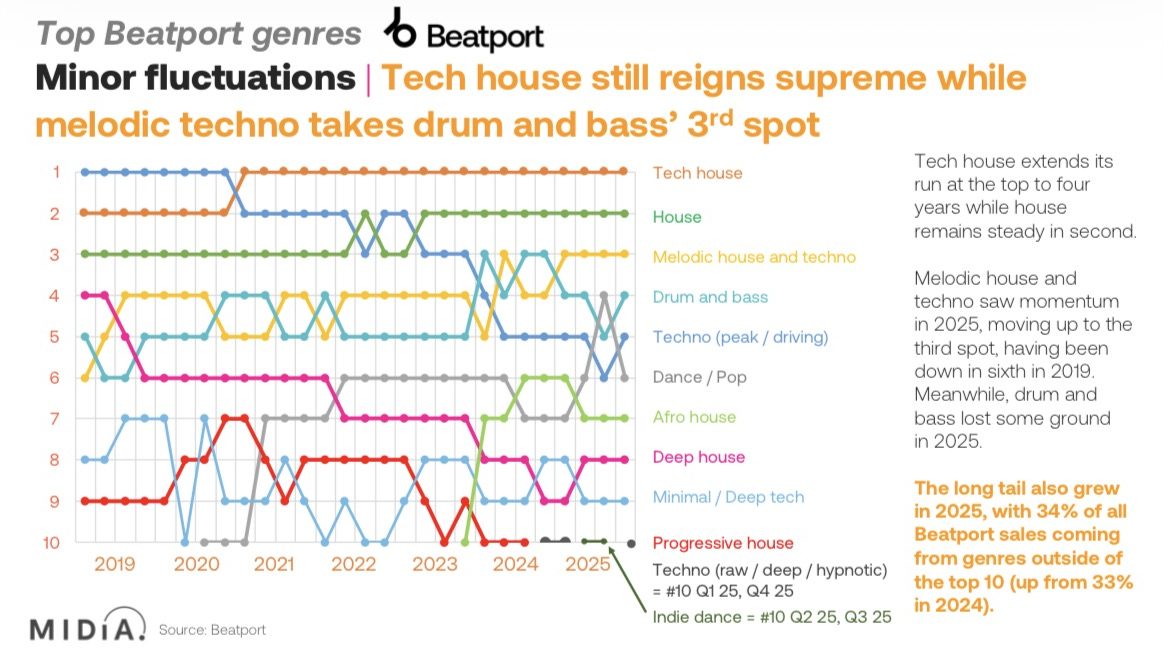

Genres and Platforms: A Data-Led View of Fragmentation

Genre-level data provides a more granular view of how electronic music is evolving across platforms. On Beatport, tech house retained the number one position for the fourth consecutive year, with house remaining second. Meanwhile, melodic house and techno climbed to third place, up from sixth in 2019—highlighting a multi-year shift rather than a sudden trend. At the same time, the long tail continues to expand: 34% of all Beatport sales in 2025 came from genres outside the top 10, up from 33% in 2024. This indicates that growth is increasingly distributed across a wider set of niche genres rather than concentrated in a few dominant categories.

Splice data reinforces this fragmentation. While trap remained the most-searched genre, Afro house rose from 10th place in 2023 to 2nd in 2025, with search volumes reaching approximately 1.3 million queries. At the same time, genres like reggaeton entered the top rankings, while others such as drill dropped out, pointing to rapid shifts in creator demand. Taken together, these trends suggest that electronic music is not moving toward a single defining sound, but toward a more diversified and decentralized genre ecosystem, where multiple styles grow in parallel across different platforms and regions.

Scenes, Not Just Streams

If there is one area where electronic music stands apart, it is in its relationship with culture. Electronic fans are more likely than average listeners to actively participate in scenes, spend more time listening to music, and engage in community-driven experiences. At the same time, global trends are becoming harder to define. Large markets increasingly shape global data, while local scenes continue to evolve independently—creating a landscape that is both global and deeply fragmented.

A More Complex Growth Model

Taken together, these shifts point to a broader transformation. The electronic music industry is no longer driven by a single engine. Instead, growth is distributed across multiple layers:

- streaming and global reach

- fandom and direct monetisation

- live experiences

- creator tools and AI

Each of these operates differently—and at a different pace.

What Comes Next

The headline number—$15.1 billion—tells a story of growth. But the more important story is how that growth is being generated. As streaming matures, the focus is shifting toward fan relationships, cultural relevance, and new forms of participation. Electronic music, with its strong scene culture, is particularly well positioned for this transition. At the same time, AI, fragmentation, and rising competition are making the ecosystem more complex. The result is an industry that is still expanding—but becoming less predictable in the process. And increasingly, success will depend not just on reaching audiences, but on understanding how they engage with music across platforms, scenes, and formats.

Rudy (32) currently based in Bergamo, here since 2019.

https://www.linkedin.com/in/rudy-cassago-522452179/