The global music industry has a new heavyweight—but this time, it is not a traditional major. With the merger of BMG and Concord now confirmed, the combined company is positioning itself as the world’s leading independent music company, and effectively the industry’s fourth-largest player. Backed by Bertelsmann with a 67% stake, and Concord’s investors holding the remaining 33%, the new entity is projected to generate around $2.2 billion in revenue and $730 million in EBITDA (Music Business Worldwide; Digital Music News). But beyond the scale, this deal represents something more fundamental: a strategic bet on a new model for how music companies compete in the streaming era.

More Than a Merger: A Strategic Alignment

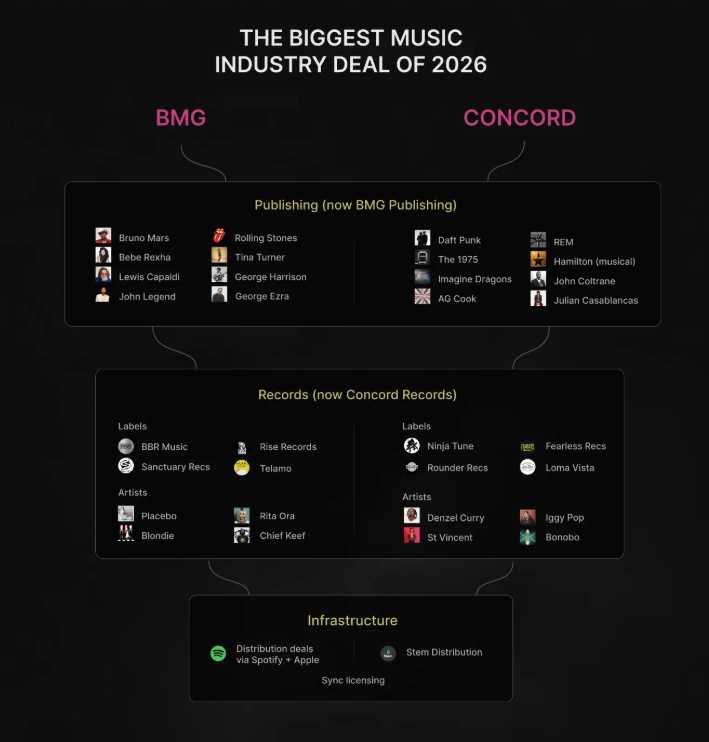

At its core, the deal is about combining complementary strengths. BMG has built its business around efficiency, rights management, and direct relationships with digital platforms. Concord, meanwhile, has focused heavily on catalog acquisition, publishing, and diversified revenue streams—including theatrical and recorded music. Together, they form a fully integrated music company, spanning publishing, recorded music, distribution, and rights exploitation—reflecting a broader industry trend where vertical integration is no longer optional, but necessary (BMG; Music Business Worldwide). The rationale is clear: scale is becoming essential, not just for growth, but for survival.

The Plan: Scale Meets Profitability

One of the most striking aspects of the merger is not just how big the company will be—but how efficiently it is expected to operate. With EBITDA margins projected at over 30%, the combined business is likely to outperform traditional major labels in profitability terms, even if it remains smaller in absolute revenue (Music Business Worldwide). This is not accidental. Executives have emphasized that the goal is to build a company that is:

- highly scalable

- operationally efficient

- and capable of reinvesting aggressively in catalog and talent

In other words, this is not a race to become the biggest—it is a race to become the most efficient large-scale player.

The “Super-Indie” Model Takes Shape

The merger highlights the emergence of a new category in the music business: the super-indie. These are companies that:

- operate at near-major scale

- are backed by institutional capital

- but maintain an independent positioning

Unlike traditional majors, the new BMG is not trying to replicate the legacy label system. Instead, the strategy is to use scale to enhance independence, offering artists more flexible deal structures while maintaining the financial and operational capabilities required to compete globally (BMG; Music Business Worldwide). This reflects a broader shift in the industry, where the distinction between “major” and “independent” is increasingly blurred.

A Capital-Driven Industry Transformation

Another key dimension of the deal is the role of capital. The transaction includes a $1.16 billion cash component, underscoring the scale of financial investment now flowing into music rights businesses (Music Business Worldwide). But more importantly, this is not just about acquiring catalogs—it is about building integrated, cash-generating platforms. Music is increasingly being treated as a long-term asset class, valued not only for its cultural relevance, but for its predictable cash flows. In this context, the BMG–Concord merger represents a shift from:

- buying music assets

to - building music infrastructure

Distribution, Technology, and AI

A critical—if less visible—part of the strategy lies in distribution and technology. BMG has already moved toward direct distribution to digital platforms, reducing reliance on third-party infrastructure. If extended across the combined company, this could significantly increase margins and strategic control (Music Business Worldwide). At the same time, executives have highlighted the role of technology and AI in driving future growth—from catalog management to operational efficiencies (BMG). This aligns with a wider industry shift, where competitive advantage is increasingly tied not just to content ownership, but to how that content is managed, monetised, and scaled.

Why This Deal Matters Now

Timing is critical. The merger comes as the music industry enters a more mature phase of the streaming era. Growth remains strong, but competition is intensifying, and scale is becoming a prerequisite for meaningful participation at the top end of the market. In this environment, the BMG–Concord deal can be seen as a response to three converging forces:

- the need for global reach in a streaming-driven market

- the importance of owning and managing large catalogs of rights

- the increasing role of technology, data, and AI in monetisation

A Market Moving on Two Fronts

At the same time, the BMG–Concord merger is unfolding against the backdrop of another potential shift in the industry. Reports have suggested that Universal Music Group is exploring a possible acquisition of Downtown Music Holdings—though no deal has been confirmed at the time of writing. If realised, such a move would point in the opposite direction: a major expanding further into independent infrastructure and services, rather than an independent scaling up to compete with majors. Taken together, the two dynamics highlight a market that is evolving on multiple fronts—where the distinction between “major” and “independent” is becoming increasingly fluid, and where scale, services, and control of rights are converging into a single competitive framework.

What Comes Next

The emergence of this new entity does not immediately disrupt the dominance of the Big Three. But it does change the structure of the market. For the first time, there is a player that:

- combines significant scale

- operates with high profitability

- and positions itself outside the traditional major label model

Whether this “super-indie” model becomes a true alternative—or eventually converges with the major system it seeks to differentiate from—remains to be seen. What is clear, however, is that the rules of competition are evolving. And in that context, the BMG–Concord merger may be less about becoming the fourth major—and more about redefining what a major can be.

Rudy (32) currently based in Bergamo, here since 2019.

https://www.linkedin.com/in/rudy-cassago-522452179/